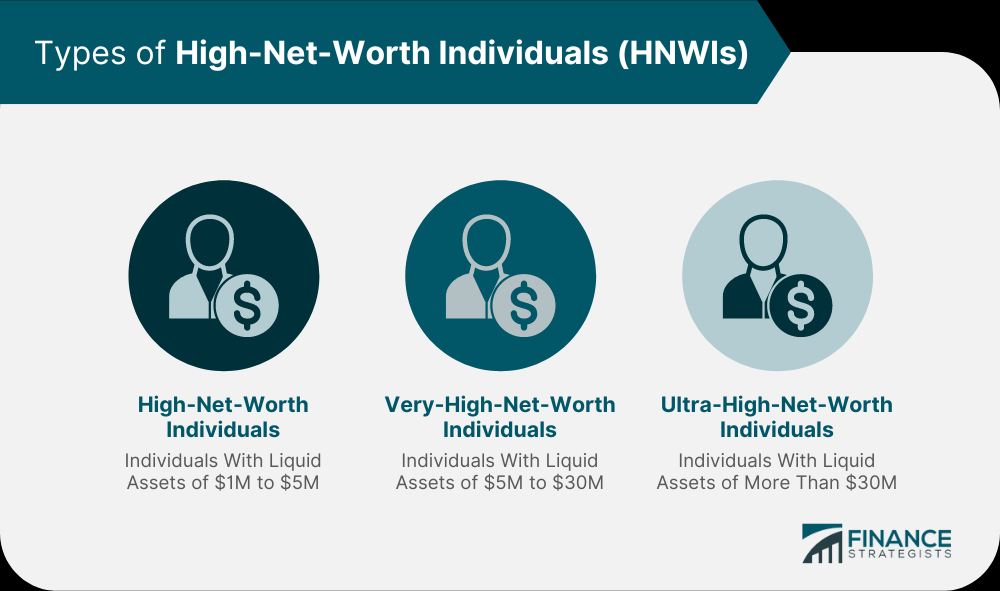

Whilst still a little subjective, a high net worth individual [HNWI] in Australia is typically defined as someone with total [net] assets of greater than $5,000,000 AUD. This could include investable assets that are greater than $2,000,000 AUD that excludes the family home [primary residence]. A global report by real estate consultancy Frank Knight states $1,000,000 USD [$1,555,000 AUD] net worth, but to get into the top 1% of high net worth Australians requires about $7,500,000 AUD.

This then begs the question, since the median house price is around $1,000,000 AUD in Australia, there are plenty of millionaires in Australia. When we get to net assets, most home loans are around 30 years, so most families pay off the family home close to age 60. This then gives the average family five to seven years to build some superannuation based on the projected retirement age. Yes, these families have assets under their control exceeding $1,000,000, their net worth is significantly less.

For a comfortable retirement, the average Australian, or Australian couple generally use their superannuation that is supplemented with the age pension. That means Australians need to wait until they are 67 before they can retire, that hurts. We have many people that have purchased rental properties [or multiple rental properties], have share accounts, crypto currency accounts, bonds and fixed interest investments. Then we have business owners [including farmers] who have sizable assets and corporate high flyers with high disposable incomes who have investment accounts that tend to hold assets.

Age Balance

25 $26,000

30 $66,500

35 $111,500

40 $168,000

45 $226,000

50 $296,000

55 $377,000

60 $469,000

65 $571,000

So for many, their superannuation is their second largest asset behind the family home. With the superannuation levy increasing to 12%, this will really be important in the future for families as younger Australians have the ability to save higher balances earlier. Baby boomers were pretty much without superannuation in their early work years. Likewise, Gen X began working with no superannuation and then began with lower contributions starting at 3%, moving to 6% then to 9% for most of their working life.