As the 2022 Retirement Income Review found, retirees were not maximising their superannuation. This is interesting, with most people retiring around age 65 and hopefully paying out their mortgage at around age 55, that gives them a decade to maximise their superannuation contributions and top-up their base superannuation to step up their retirement savings.

Based on what I have read, clients are signing onto retirement advisors when they close to or entering retirement, owning their own house with typically with about $1m to $1.5m in super and other assets. However, plenty are in a cold sweat from the very rational fear that they will outlive their retirement savings. If you own a million dollar property and have close to half a million in superannuation, then you are doing ok.

What we are now witnessing is retirees have died substantially wealthier than when they began retirement – imagine that. I read about a client who was substantially richer to the tune of two-and-a-half times after 25 years in retirement – not bad. That is what I will be seeking to replicate, having a retirement drawdown that is replenished by earnings. Since we have had compulsory superannuation in Australia since the early 1990s starting at 3%, moving to 6% and then 9% so plenty of us worked without cover for a while, but at least we have something.

Whilst this is an American model, does the 10:30:60 model work in Australia? Firstly, what is this model? 10% of your retirement savings comes from contributions during your work life, 30% comes from investment income during the accumulation phase and 60% of earnings comes down during the drawdown phase in retirement. The model was developed by Don Ezra at Russell Investments in 1989 when double digit returns were the norm during times of lower inflation.

Therefore, you need to have your investments set for growth even in retirement with some defensive earning assets such as bonds and fixed interest. The 10:30:60 rule suggests 90% of your retirement funds come from investments, is this really true? According to sources, a 15:31:54 split is more likely in Australia. Even with compulsory superannuation, if you can match employer contributions for a period of 10 years then you double your contributions for an extended period. This makes a massive improvement to your retirement account improving the final payout.

I do not want to wait until I reach age 65 to stop working, I want to travel again and enjoy myself, sure I will try to pick up some part time work to contribute to my retirement income. I certainly do not want to clock-on and clock-off and not be fully engaged in the job. I have a work ethic, but what I want is to disassociate my life from the job, this is something that I am not doing now. I can absolutely report that I will not be waiting until I am 67, the official retirement age where I can claim a pension, I currently do not qualify for the pension so I will have to wait a long time until I have drawn down my pension to a level where I can qualify for the age pension.

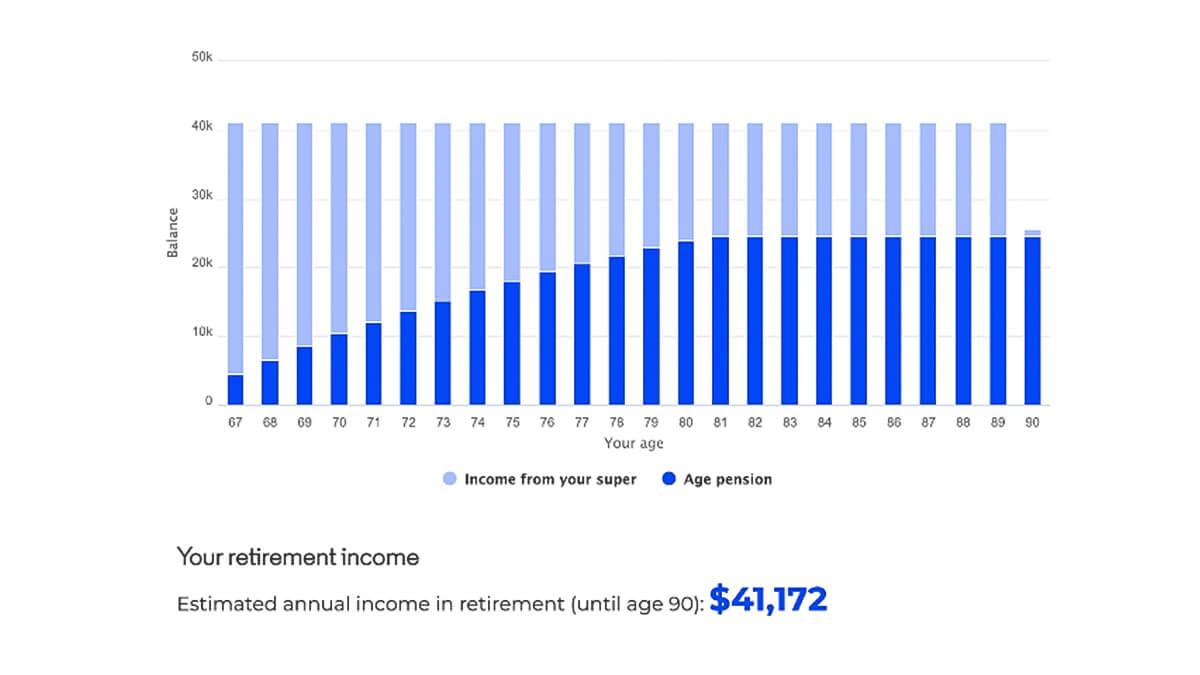

Whilst fears of longevity risk may be somewhat overblown, in Australia you can claim the pension when you have exhausted your retirement savings – you will not be totally without income. I do understand there is a proportion of the population living below the poverty line, there are homeless people and this is not always of their own doing. There are pressing concerns for the retirees, this is more related to health issues as they age, there are costs involved and they do have to be accounted for.

The drawdown will be higher in the earlier years, you are more active and get out and about, you drop the costs of travel to and from work with associated costs. People like to travel and they should, you have worked a lifetime and should now be supported by a system they supported in their working lives. As their superannuation runs down, they can claim a part pension to supplement their income, I think this is a fair system. Like many people, I may not be in a cold sweat but I am certainly concerned about the longevity of my retirement account.